Marketing Strategy vs. Marketing Plan? (The Difference)

A company’s success relies heavily on the right marketing strategy supported by a robust marketing plan. That said, beginning marketers […]

Read More »Become a successful marketing consultant: Learn more

If you haven’t heard of LIBOR vs SOFR, you are in for a treat.

That’s because these two seemingly simple acronyms can literally be the difference between having plenty of excess funds for your marketing growth strategy versus not.

In this article we will briefly explain what LIBOR vs SOFR means and how it impacts your marketing.

What is LIBOR vs SOFR?

LIBOR is the London InterBank Offered Rate and SOFR is the Secured Overnight Financing Rate. LIBOR is an interest rate set by a group of bankers out of London. SOFR is the rate at which financial institutions borrow U.S. dollars. With LIBOR loans, unsecured borrowing is practiced, whereas SOFR is based on secured borrowing.

The financial industry is leaving LIBOR and adapting to SOFR.

What does this mean to the idea of globalization, the deglobalization trend and ultimately how does it affect your marketing plans?

More than you might think.

As we dig into this highly important topic, it is suggested that you briefly review these helpful articles:

Ok, now, let's briefly describe LIBOR vs SOFR.

Don't worry if this is new to you. Ultimately it’s very simple and has to do with 1) the cost of borrowing capital and 2) who is in charge of setting the rates for financing your capital needs.

This is really why it affects almost every business in the United States, and even a large part of the world.

As we get into this very important topic of obtaining funds for your marketing, you might want to review these topics so the ideas are fresh on your mind:

Ok, let’s start by understanding the LIBOR and SOFR terms and run through a couple simple examples.

LIBOR is a set of benchmark interest rates calculated from submissions by large global banks such as Barclays, Deutsche Bank, and UBS.

LIBOR rates are supposed to represent the cost of borrowing among the banks.

It is estimated that LIBOR served as the benchmark rate in more than $200 trillion worth of contracts worldwide. Over-the-counter and exchange-traded derivatives account for most of this estimated exposure to LIBOR. LIBOR is also referenced in trillions of dollars worth of business and consumer loans, mortgages, bonds, securitizations, and nonfinancial corporate contracts.

In fact, every time you and I:

... A percentage of our hard work and income we earned to pay these loans sent to the LIBOR bankers out of Europe.

For more on this, review these two helpful articles:

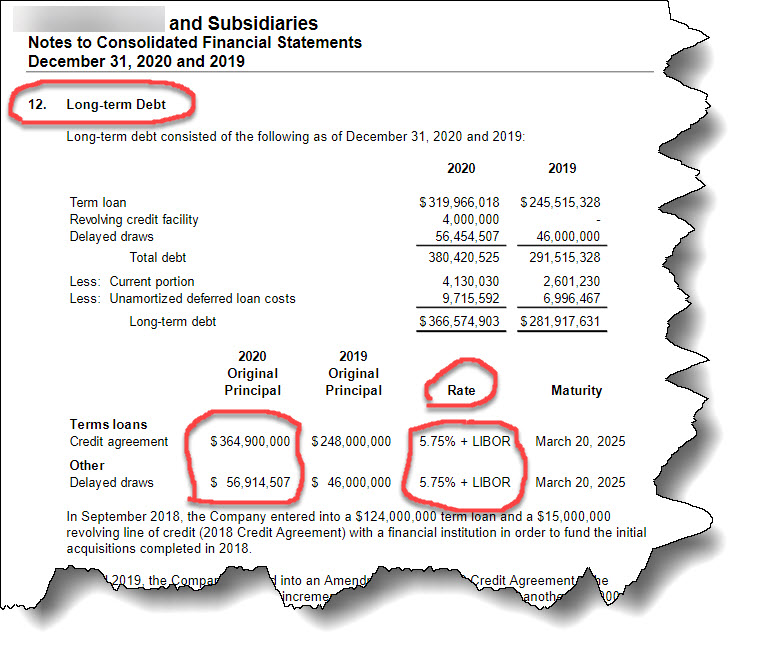

Back to the business of marketing. Below is a real example of a LIBOR loan to one of the largest franchises in the United States that specializes in home health care. This is one small example of how a lot of businesses fund their operations, and directly affects marketing departments across the country. This example is taken from the notes in this particular franchise's Financial Statement under Item 21, in their Franchise Disclosure Documents (FDD).

This is important because it represents nearly $400 million in long term debt based on LIBOR rates, again, set by a group of bankers with representation out of London.

Again, these LIBOR rates are not set by American banks. In fact, American banks including the Federal Reserve have little to no control over LIBOR rates.

Here is another real example taken from the Franchise Disclosure Documents (FDD) from another one of the largest home health care service providers in the United States. This paragraph is taken from the notes in their Financial Statement under Item 21. What this is showing is their loan is based on a LIBOR rate subject to a minimum rate of 1.00% plus base rate and additional rates stacked on top of this.

This company has a term loan of about $62 million plus a $5 million line of credit (LOC). This means that the LIBOR banks, with representation centered in London making decisions with no collateral needed to set the rates on these funds.

SOFR is the average rate at which financial institutions can borrow U.S. dollars overnight while posting U.S. Treasury bonds as collateral.

Similar in nature to a mortgage, SOFR is a secured borrowing rate because collateral is presented to borrow cash. SOFR differs from LIBOR in that in LIBOR; no collateral is shown to borrow cash, meaning that it is unsecured borrowing, whereas SOFR is secured borrowing.

New York Fed calculates Secured Overnight Financing Rate (SOFR) by taking the volume-weighted median of transactions in three markets for repurchase agreements collateralized by U.S. Treasury securities. The transaction volumes underlying SOFR regularly are around $1 trillion daily.

Below is a screenshot of J.P.Morgan Chase and their communication of the transition away from LIBOR and into SOFR.

Interestingly, if you are interested in reviewing your Customer Value Proposition, specifically Operational Excellence as opposed to Product Leadership or Customer Intimacy, we featured some explanations about JPMorgan Chase and McDonalds here:

What is Operational Excellence and Why is it Important?

This table will give you a better understanding of the critical differences between SOFR and LIBOR rates.

| Basis | LIBOR | SOFR |

| Benchmark | This rate is used as a benchmark to set the interest rates for various financial instruments globally. | It is a benchmark interest rate that depends on the U.S. Treasury repurchase agreements. |

| Estimation | Depends upon the average daily estimates for borrowing rates. | Depends upon actual borrowing rates or the transactional data. |

| Period Consideration | Estimate rates for seven borrowing periods (Overnight to 12 months) | Limited to overnight transactions. |

| Risk | It carries the credit risk of taking a loan from the bank. | Risk-free rate. |

| Accuracy | It is less accurate as it is based on estimates and assumptions. | It is more accurate as it depends upon actual transactions. |

| Secured | Unsecured. | Secured with the U.S. Treasury. |

| Currencies | USD, JPY, CHF, GBP, and EUR. | Includes only USD. |

| Rate | Forward-looking rate | Backward-looking rate. |

| Transactions | Based on roughly $1B transactions daily. | Based on roughly $1T transactions daily. |

The London Interbank Offer Rate (LIBOR) dominated the financial industry for about 50 years but now it's time has come to an end. It’s very interesting to note that this is about the same time the petrodollar and the Eurodollar started to gain traction.

Some possible reasons for the transition from LIBOR to SOFR are as follows:

These four points will summarize why we are switching from LIBOR to SOFR:

In summary, the change to SOFR is based on actual interest rates in the United States and backed by the US Treasury.

LIBOR, on the other hand, is set by a few bankers out of London with no collateral to support their decisions.

If we didn’t know better, LIBOR in itself would seem like a flawed, almost fraudulent method of how these European banks, largely operated out of London, Germany and The Netherlands (the same banks that have run the world since the first stock market exchange in the 1600’s and have funded global communications, education initiatives, trade monopolies, regime changes on and on), earn interest income out of thin air on the backs of the productive people of the United States.

But of course we know this is not the case because they earn income based on the Eurocurrency and Eurodollars. It is highly suggested that you learn more about the Eurodollar here (yes, there is a lot more to this story and how it affects your marketing strategies).

SOFR on the other hand is based on actual United States transactions and removes itself from the currency turmoil found in London, Germany and The Netherlands, as an example.

At the end of the day, what this really means is that when a local home health care provider is helping your grandparents, who devoted their life to helping others in the community they love, they aren't supporting immoral, unethical behavior that potentially funded the LIBOR decision makers.

Yet another reason why a quality marketer should always choose Free Enterprise where the market decides what is best, as opposed to a small group dictating policy.

References: